Budgeting and understanding where your money is going can make all the difference. When it comes to keeping tabs on your cash flow, it’s vital to get a good grasp on two things: income and expenses. This means breaking down everything, from your paycheck to any side hustles you might have.

QUICK LOOK: – 7 Tips for Managing Your Personal Finances

- Building up an emergency fund is like having your very own safety net for those unexpected life hiccups. It’s all about being ready for those just-in-case moments—like an unplanned car repair or sudden medical bill—that could otherwise throw your finances off course.

- Tackling debt might seem overwhelming, but it’s crucial for regaining control over your finances. The first step is to get a handle on what you owe and prioritize which debts to tackle first.

- Getting a head start with investing is one of the smartest moves you can make for your financial future. The earlier you start, the more you can leverage the power of compounding interest to grow your wealth over time.

- Regularly checking your credit reports helps ensure all the information is accurate and up-to-date. Mistakes can happen, and catching errors early can prevent future headaches.

- Retirement might seem a long way off, but planning ahead can make all the difference in the quality of your life later on. Start by contributing to retirement accounts like a 401(k) or an IRA. If your employer offers a matching contribution, try to maximize it.

- Embracing the habit of living below your means can be transformative for your financial health. It’s all about making mindful spending choices and ensuring you aren’t stretching your earnings too thin.

- Staying informed about personal finance is a lifelong journey that can significantly shape your financial success. There’s always new information to learn, whether from books, blogs, podcasts, or online seminars. Constantly updating your financial knowledge ensures you’re prepared for whatever economic changes come your way.

On the other hand, expenses aren’t just the big stuff like rent or groceries; it’s also about those sneaky extras like coffee runs or takeaway meals. Recognizing every penny in and out is the foundation of a solid budget. Once you know where your money is headed, it’s time to set some financial goals. These goals act like a roadmap, guiding your spending and saving.

Whether you’re eyeing that summer vacation or beefing up your retirement fund, having clear, achievable targets helps focus your efforts. Think short-term gains and long-term ambitions. Both have a place in a well-rounded financial strategy, and they’ll keep you motivated when the going gets tough.

However, crafting a budget isn’t a set-it-and-forget-it deal. Regular check-ins are crucial. Life isn’t static, and neither is your financial situation. Maybe you got a raise, or your rent went up. Adjusting your budget not only ensures it mirrors your current life but also reinforces good money habits. These tweaks keep you on track for those goals, whether you’re looking to save a little extra each month or cut back on unnecessary expenses.

Budgeting 101 – Establishing Your Emergency Fund

Building up an emergency fund is like having your very own safety net for those unexpected life hiccups. It’s all about being ready for those just-in-case moments—like an unplanned car repair or sudden medical bill—that could otherwise throw your finances off course.

Starting small is perfectly okay. The idea is to aim for saving enough to cover at least three to six months’ worth of living expenses. This might look like a big mountain to climb, but taking it step by step makes the goal much more achievable. Setting realistic targets for yourself and saving a little bit each month can really add up over time.

Automation can seriously be your best friend when it comes to saving. By setting up automatic transfers from your checking to your savings account, you take the guesswork out of saving. It’s a hassle-free way to make sure you’re consistently setting aside funds—and you’ll be surprised at how painless it can be. Treat it like any other bill that you pay every month to reinforce the habit of saving.

Budgeting 101 – Strategies for Debt Reduction

- Tackling debt might seem overwhelming, but it’s crucial for regaining control over your finances. The first step is to get a handle on what you owe and prioritize which debts to tackle first. High-interest debt should be at the top of your list—think credit cards and personal loans. These can snowball quickly, so directing any extra cash toward these can help shrink them faster.

- Living within your means is another essential strategy. This requires a bit of restraint and careful planning, but the payoff is huge when you can avoid taking on more debt. Sticking to your budget helps in this regard, ensuring that you’re not spending beyond what you earn.

- Setting up a structured repayment plan is key. Listing your debts and deciding on a method, like the avalanche or snowball method, can offer a clear path forward. The avalanche method focuses on paying off the highest interest rates first, while the snowball method builds momentum by knocking out the smallest debts. Choose what works best for you and keep your eyes on the goal: living debt-free.

Budgeting 101 – Mastering the Investment Game

Getting a head start with investing is one of the smartest moves you can make for your financial future. The earlier you start, the more you can leverage the power of compounding interest to grow your wealth over time. It’s not about having a ton of cash to invest right away; it’s about letting time work its magic on whatever amount you can manage.

Diversifying your portfolio is crucial to minimize risk and safeguard your investments. This means spreading your money between different asset classes, such as stocks, bonds, and real estate. By not putting all your eggs in one basket, you reduce the impact of a downturn in any single market.

If navigating the financial markets feels daunting, there’s no shame in consulting a professional. Financial advisors can offer valuable insights tailored to your personal situation, helping you make informed decisions. Seeking expert advice could be the difference between a successful investment strategy and one fraught with unnecessary risks.

Budgeting 101 – Keeping a Close Eye on Your Credit

Understanding your credit health can open doors to many financial opportunities, so it’s vital to keep a close watch over it.

- Regularly checking your credit reports helps ensure all the information is accurate and up-to-date. Mistakes can happen, and catching errors early can prevent future headaches.

- To keep your credit in good shape, aim to manage credit cards wisely. This means not letting balances pile up and making sure you pay off at least the minimum due every month. Timely payments are one of the most significant ways to boost your credit score, showing lenders you’re reliable.

- Improving your credit score isn’t just about paying bills on time. It’s also about keeping old accounts open and avoiding unnecessary credit applications. Both can positively influence your score, making it easier for you to secure loans or get better interest rates when needed. Taking small, deliberate steps can steadily improve your financial standing.

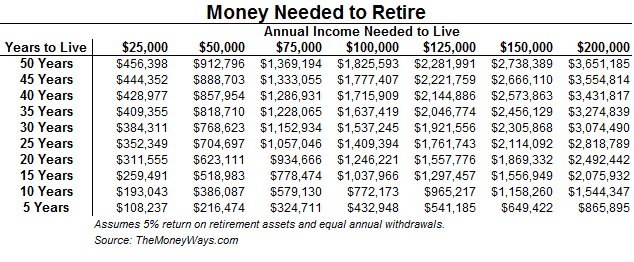

Budgeting 101 – Preparing for a Comfortable Retirement

Retirement might seem a long way off, but planning ahead can make all the difference in the quality of your life later on. Start by contributing to retirement accounts like a 401(k) or an IRA. If your employer offers a matching contribution, try to maximize it. That’s essentially free money contributing to your nest egg.

Understanding the differences between various retirement accounts can help you make informed decisions. A 401(k) typically comes from your employer, while an IRA is more of a personal choice. Each has unique advantages regarding taxes and withdrawal conditions, so knowing which suits your situation best is crucial.

Setting clear retirement goals is about envisioning how you want to live your golden years. Think about your lifestyle expectations and expenses. Maybe you dream of traveling or enjoying hobbies full-time. Planning now ensures you’ll have the funds to support those dreams without financial stress.

Budgeting 101 – Living Below Your Means Financial Discipline

- Embracing the habit of living below your means can be transformative for your financial health. It’s all about making mindful spending choices and ensuring you aren’t stretching your earnings too thin.

- Understanding the difference between needs and wants is crucial. Needs are essential expenses—like housing, utilities, and groceries—while wants include those nice-to-have items such as the latest gadgets or dining out frequently. Prioritizing essentials allows you to manage your cash flow more effectively.

- Impulse purchases can strain your budget without you even realizing it. Before making a purchase, especially a significant one, ask yourself if it’s something you truly need or just a passing desire.

- Adopting a frugal mindset doesn’t mean you’re depriving yourself. Rather, it’s about finding more cost-effective ways to enjoy the things you love. This discipline can lead to greater financial stability and prepare you for any future opportunities requiring a financial outlay.

Budgeting 101 Final Analysis – Continual Financial Education and Review

Staying informed about personal finance is a lifelong journey that can significantly shape your financial success. There’s always new information to learn, whether from books, blogs, podcasts, or online seminars. Constantly updating your financial knowledge ensures you’re prepared for whatever economic changes come your way.

Looking to others who are financially savvy can provide both inspiration and practical knowledge. Whether it’s friends, family, or mentors, learning from their experiences and insights gives you a broader perspective and potentially valuable advice.

Regular reviews of your budgeting and financial plan are vital. Life changes, and your financial strategy should adapt in tandem. Perhaps your income has increased or you’ve had a change in expenses. Regularly evaluating your plan lets you make necessary adjustments, keeping you aligned with your goals and ensuring ongoing growth.

Celebrate your milestones, no matter how small. Each achievement boosts your motivation and acts as a reminder of where you started and how far you’ve come. Appreciating these wins is an encouragement to stay the course and continue managing your money effectively.

Check Out Our Latest Articles:

- Affordable Studio Lighting Kits To Level Up Your Video Content

- Optimizing Blog Posts For GEO To Boost Affiliate Revenue

- Profitable Full-Time Blogging with Diversified Income Streams

- Increasing Engagement To Boost Affiliate Marketing Income

- Scaling Content Production Without Increasing Costs

- Balancing Content Quality And Posting Frequency

Wishing You Much Success in Your Budgeting,

- onlinebenjamins.com

- thebeachangler.com

- thesinnerinthemirror.com

- Facebook: Online Benjamins

- Twitter: @onlinebenjamin1

- Instagram: dotcomdinero

- YouTube: Online Benjamins

Rex

P.S. If you have any questions or are unsure of anything, I am here and I promise I will get back to you on all of your questions and comments. Just leave them below in the comment section. Follow me on Twitter: @onlinebenjamin1, Instagram: dotcomdinero, and Facebook: Online Benjamins

Hi,

Thanks for stopping by and congratulations for taking the first steps to building your own online business. I’ve been in business both offline and online since 1997. I would consider it an honor to help you build your business. Father of 3, life long outdoorsman with an education in Genetics and Economics. This site is about cutting through the BS and finding the real opportunities in the online world. I look forward to working with you.